Know where you’re going

So now that you know where you are, you can figure out where you’re going. Based on your starting point, think about what a realistic goal would be for the new year. Your goal should be specific and achievable. While the goal of dropping 100 pounds in a year is specific, it’s likely not achievable if you only weigh 200 pounds. Similarly, setting a goal to pay off all of your debt this year is specific but not achievable if you have $200,000 in debt.

Let’s look at some examples of more realistic goals. If you’ve been paying your debt down by $2,000 per year, maybe set a goal to pay off $5,000 this year. If you’ve been able to save $500 a month into your 401(k), maybe set a goal of $800 a month. Like most goals, financial goals that stretch you are a good thing, but the bigger the stretch the more motivation you will need to get there.

Figure out how to get there

Now that you have starting and end points, you get to do some arithmetic to figure out how to get there. For single-year goals this is simple, but for longer-term goals the time value of money comes into play both for your savings as they grow based on your return, and for the inflation of the cost of your goal.

For now we’re just worried about the short-term goals. So if you want to go on a $2,500 ski trip at the end of next year, and you currently have $500 saved for travel, you’ll need to save $2,000 over 12 months, or $167 each month. If you put that money in an online savings account (as of me writing this Ally Bank is currently paying 1.25% on savings accounts), then you actually only need to save $165 each month to meet the goal.

Track your progress

With your plan in place, you now need to track how you’re doing on a regular basis. Monthly makes sense for most financial goals, unless you’re paid on a different frequency and you think about your budget bi-weekly, semi-monthly, or some other way. Put it in writing in a place where you see it often, like a post-it on your fridge or desk with your target and your current progress. For me I have a target for side-hustle earnings while I get my company up and running. I keep a running tally of my daily earnings against my goal on the back of a gas receipt in the car so that I can stay motivated and know when I’m having a good week, and when I’ll need to put in some extra time to reach my goal.

Have some fun

Make sure that your financial goals don’t strip all of the fun out of your life. Even when on a really strict budget, my wife and I have each had a little bit of fun money so we could go have coffee with friends, or save up to buy a new game. If you cut out all of the fun during the year, you run the risk of feeling trapped and demoralized when you’re not making progress as quickly as you’d like and then going on a spending spree and ruining any chance you had of meeting your goal. Think of the fun money as a small safety valve to keep that from happening.

Possible Practical Goals for 2018

If you’re having trouble thinking of financial goals to set for yourself for 2018 here are some generic goals to help:

Contribute $____ / ___% more each month to my 401(k)

Save $______ for a vacation with _________ to _________

Reduce my debt by $_____ / ___% during the year

Reduce spending on _______ by $_____ each month

Track my spending for ____ months then establish a budget (don’t forget to include once-a-year expenses)

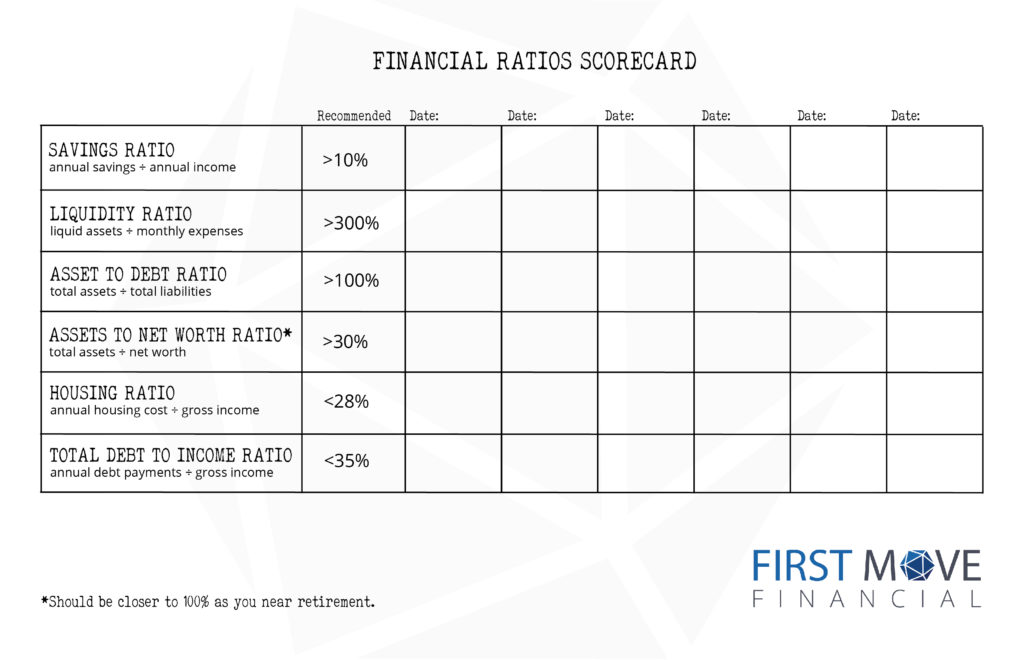

I also have a Financial Ratios Scorecard that I use with clients. Here’s a copy so you can track your progress in these key areas.

Download: Financial Ratios Scorecard